by Hazel Henderson

©2020 Hazel Henderson

Today the money meme rules our lives and social interactions in most societies on Earth. How did this happen? I studied all the economics textbooks of every perspective from the Austrian “laissez-faire” market fundamentalists to Adam Smith’s Wealth of Nations, (1776) and his earlier Theory of Moral Sentiments, (1759), as well as Karl Marx, who claimed not to be an economist. From Karl Polanyi’s broader views, I learned that trading was innate in human behavior and how indigenous peoples in the South Pacific traded shells in their canoe travels and visits among these islands in “Primitive, Archaic and Modern Economics, (1968). In Polanyi’s “The Great Transformation, (1944), I learned how traditional societies and local market norms in communitarian village life were over-ruled by legislation in the British parliament which created national markets and facilitated global trade and colonial exploitation as these markets expanded. I was fortunate to know Polanyi personally and visited his wife Ilona at their home in Toronto. My efforts to expose this historic story and its contemporary outcomes began with “Creating Alternative Futures: The End of Economics” (1978, 1996, 2014). And “The Politics of the Solar Age” (1981, 1988), now in 800 libraries in 20 languages.

I learned growing up in the city of Bristol, a key port in Britain’s slave trade, in a typically patriarchal family, that money is a tool of power. Money is now widely used in most countries to control and incentivize human behavior, of individuals, families and communities to cities, nations, steering technology choices and industrialism internationally in what I termed today’s “global casino”. My father kept my wonderfully loving mother penniless, making her grovel for cash to pay our grocery bills, while he dined out and golfed with his fellow business leaders. In Britain at that time, men were dominant and women were subservient. Fathers were kings in their home “castles”, as I experienced, with wives and children obeying, often with punishment and domestic violence. This gender-based caste system, reinforced by controlling the money-meme, still is widespread. When I and my sister would try to call the police, my mother would say “No, no-one must know about this!”. We asked if we could all run away, but our distraught mother replied, “My dears, we can’t because I don’t have any money”. At age 16, I left home and found an entry level job, joining my elder sister in a cheap youth hostel she had found. Such conditions of domestic violence and coercion are reflected in the personal account of US Poet Laureate Natasha Trethewey in “Memorial Drive“ (2020), and by Dr. Monica Sharma, Indian physician advisor to the United Nations (UN) in her “Radical Transformational Leadership” (2018)

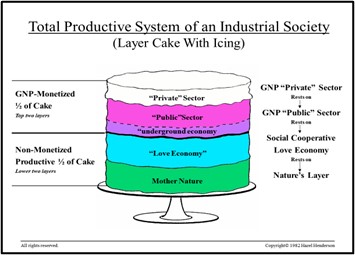

This familiar childhood experience of millions, drove my fascination to unravel this controlling money meme and how it  limited our freedom and life choices. Thus, my first two books studied the non-money, unpaid traditional community sharing of goods, services and mutual aid. Raising children, as Hillary Clinton describes in “It Takes A Village” (2017) requires loving unpaid care, in maintaining households, service on voluntary programs like Meals on Wheels and the free Well-Baby Clinic as my mother did. I called these un-counted sectors underpinning all societies “Love Economies”. While they buttressed all societies, the money metrics overlook them, and economic textbooks call them “un-economic”. Indeed, these textbooks describe human nature as selfish and competitive, while deeming volunteering as “irrational”. My “Cake” visualizes the expanded total production in all societies, including the unpaid Love Economy and Nature’s services in our shared biosphere, photosynthesizing the daily free photons from our Sun in creating our food, shelter and survival.

limited our freedom and life choices. Thus, my first two books studied the non-money, unpaid traditional community sharing of goods, services and mutual aid. Raising children, as Hillary Clinton describes in “It Takes A Village” (2017) requires loving unpaid care, in maintaining households, service on voluntary programs like Meals on Wheels and the free Well-Baby Clinic as my mother did. I called these un-counted sectors underpinning all societies “Love Economies”. While they buttressed all societies, the money metrics overlook them, and economic textbooks call them “un-economic”. Indeed, these textbooks describe human nature as selfish and competitive, while deeming volunteering as “irrational”. My “Cake” visualizes the expanded total production in all societies, including the unpaid Love Economy and Nature’s services in our shared biosphere, photosynthesizing the daily free photons from our Sun in creating our food, shelter and survival.

I found an ally in Marilyn Waring, a New Zealand parliamentarian, in her “If Women Counted” (1988) which became a perennial best-seller among the world’s women. By 1995, I had helped persuade the United Nations Human Development Program (UNDP) to look at this unpaid half of all societies in their Human Development Index , (HDI) reports. They estimated that $16 trillion worth of these unpaid goods and services ($11 trillion by women and $5 trillion by men) was simply missing from that annual GDP of $24 trillion in 1995. If this unpaid production had been added, that year’s GDP would have risen to $40 trillion, (www.undp.org).

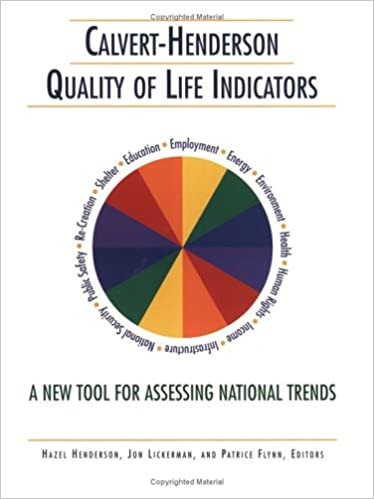

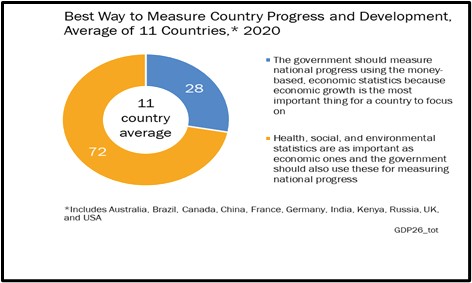

By 1982, after my self-education as a civic leader in New York City’s Citizens for Clean Air and six years as a government science policy advisor, I was invited to serve as a member of the Calvert group of socially-responsible mutual funds’ advisory council. In 2000, we jointly launched the Calvert-Henderson Quality of Life Indicators, measuring values beyond money, using the scientific data on 12 aspects of Quality of Life. In 2004 I founded Ethical Markets Media, and in 2007, launched with GlobeScan, global polling on “Beyond GDP” in twelve countries. We asked whether their publics favored either keeping the money-based GDP as the measure of national progress or to expand it with real-world data on health, education and environment. In our series in 2009, 2013 and our 2020 survey, we still find an average 72% favoring expanding GDP. Thus, people are way ahead of politicians and economists in understanding the limits of the money meme of GDP.

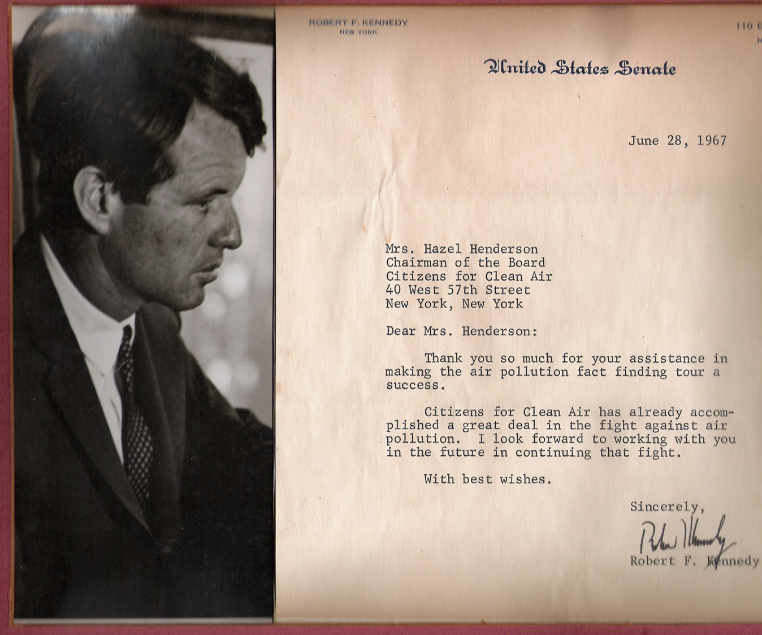

Citizens for Clean Air advocated correcting GDP by subtracting the “bads” of pollution from the “goods”. Our ally, Senator Robert Kennedy, whom we took on a helicopter ride to see New York’s air pollution emissions, spoke  eloquently of how GDP “measured only money transactions and ignoring everything we hold dear”.

eloquently of how GDP “measured only money transactions and ignoring everything we hold dear”.

As a writer, critic, community organizer and activist, I always emphasized that money was not wealth, but simply information. Yet, the money meme is used as the ubiquitous metric for keeping track and scoring our human goals and activities. Money is merely a numeraire, like inches, feet, hectares and centimeters. Looking around the world, I found that many communities understood this and had decided that if their nation’s central bank, the “big croupier” was not going to create enough money chips for them to complete their local trades and employ their own citizens on local tasks, that they would simply create chips of their own. These local currencies are still thriving all over the world wherever central banks keep the money supply too tight or governments impose “austerity”, or mismanage the design of their economic rules. The most famous are the “Berkshares” created decades ago in Great Barrington, Massachusetts, designed by the late Robert Swan and Susan Witt, who still heads the Schumacher Society, (www.centerforneweconomics.org) there. Most of the local banks accept Berkshares and they allow many enterprises to flourish, creating community supported agriculture, co-housing and all the local new businesses and restaurants financed initially by Berkshares. People have two currencies: Berkshares in one pocket for local use and US dollars in the other pocket for buying goods and services from the national marketplace.

In early 2008, Ethical Markets co-produced with independent monetary theorist and filmmaker, Alan Rosenblith,  our TV special “The Money Fix”, which dives into the murky politics of money-creation and credit-allocation. In its second half-hour, we cover local currencies, including Berkshares, as well as local barter systems. Now most are online such as E-Bay, Craigslist, and many other swap sites. We begin this TV show by asking people on the street if they knew where money came from. Most had never thought about it —- just as fish do not notice the water they swim in. One young woman told us that money was produced in a big factory in order to control us. Others saw it as central in their lives. This TV show has been aired on about 50% of the PBS affiliated TV stations in the USA, via our independent satellite feed, distributed globally to colleges at www.films.com and also free on demand with many others in our “Transforming Finance” series at www.ethicalmarkets.tv. Many tell us our TV shows help release them from the conceptual prison of the money MEME. Millions in many countries have now withdrawn from the consumer rat race to focus on their precious time and deeper key values and goals, as reported by our colleague Vicki Robin in her perennial best-seller “Your Money or Your Life” (2008). My conversations with Vicki are also on “Money Or Life” (2018), “Your Money or Your Life”, (Oct 8th).

our TV special “The Money Fix”, which dives into the murky politics of money-creation and credit-allocation. In its second half-hour, we cover local currencies, including Berkshares, as well as local barter systems. Now most are online such as E-Bay, Craigslist, and many other swap sites. We begin this TV show by asking people on the street if they knew where money came from. Most had never thought about it —- just as fish do not notice the water they swim in. One young woman told us that money was produced in a big factory in order to control us. Others saw it as central in their lives. This TV show has been aired on about 50% of the PBS affiliated TV stations in the USA, via our independent satellite feed, distributed globally to colleges at www.films.com and also free on demand with many others in our “Transforming Finance” series at www.ethicalmarkets.tv. Many tell us our TV shows help release them from the conceptual prison of the money MEME. Millions in many countries have now withdrawn from the consumer rat race to focus on their precious time and deeper key values and goals, as reported by our colleague Vicki Robin in her perennial best-seller “Your Money or Your Life” (2008). My conversations with Vicki are also on “Money Or Life” (2018), “Your Money or Your Life”, (Oct 8th).

So how did this money meme take over our societies and get installed in the hard drives of all our institutions’ operating systems? Our free TV show, “The Money Fix” explains how the power to coin our USA money based in our Constitution, fell into private hands, as bankers and their political allies created the Federal Reserve in 1913. While the Fed does have a publicly appointed chair and members of its Federal Reserve Board, it remains a private institution. Recently, current Fed chair Jerome Powell was asked on the CBS TV show “60 Minutes” the usual dumb question asked whenever anyone proposes any public sector program “Where’s the money coming from?”. Powell responded that the Fed prints its, not just the banknotes, but also digitally in its computer databases and programs. Essentially, the Fed simply moves some of the decimal points! All this is tracked in Bloomberg Businessweek’s successive articles including, “When Hawks Cry”, Oct. 12, 2020, and the Economist, July 25, 2020.

In truth, money isn’t scarce and all sovereign governments create it, whether US dollars, Japanese yen, China’s yuan and Britain’s pound. All their central banks empower their commercial banks to create money every time they make a loan or mortgage for a borrower. The bank makes a new numerical entry of the loan amount into the borrower’s account. Then the textbook rules of “fractional reserve banking“ followed by most central banks allow these commercial banks to turn around and make additional loans of up to ten times their digitally- stated reserves on their books. The Bank of England has now made this process public after pressure from civic groups and money reformers including Positive Money, and our partners in the Green Economy Coalition and by Joseph Huber in “Sovereign Money”, (2018).

This money-creation process is rarely documented in economic textbooks. Most accept money as a given: an accounting unit, a means of exchange and a store of value. Today, as I pointed out in “Money Is Not Wealth: Cryptos v. Fiats”, our currencies, if well managed can still be useful mediums of exchange. But they are subjected to trillions of speculative traders pyramiding assets in derivatives on ballooning global FOREX markets, so currencies are no longer are a dependable store of value. Efforts to curb this currency speculation include taxing all financial transactions, as proposed by economists James Tobin and later by Lawrence Summers, to “throw sand in the gears” (Summers, 1987). Ethical Markets devised a computer program, FXTRS to collect these financial trading, algorithms driving robot investment advice and negative financial transaction taxes and add the huge proceeds to the currency stabilization fund of countries’ under attack. (Henderson and Kay, “Foreign Exchange Transaction Reporting System”, FUTURES, 1996).

Today, with still untaxed financial trading algorithms driving robot investment advice and negative interest rates, people have few investment choices. They are forced into stock markets dominated by computer trading and unregulated cryptocurrencies, or hoarding cash in their mattresses! Since the financial meltdown of 2008, many computer-driven “flash crashes” followed, due to high-frequency trading described by Michael Lewis in” Flash Boys” (2013), and in my “Perspectives on Reforming Electronic Markets and Trading”, (2014), for the UN Inquiry on Sustainable Finance, (www.unepinquiry.org).

Most people understand that central banks create our money and often coordinate their policy and actions, as described by former Goldman Sachs managing director, Nomi Prins in “Collusion“, (2018). During financial crises, they increase the money supply in their programs of “Quantitative Easing” (QE), adding this new money by buying up dud mortgage-backed securities created by reckless bankers. The textbook theory says that this new money will “trickle-down” to fund the trading and investment purposes in the real world,” Main Street “economies. In today’s globalized money-measured GDP regimes, this new money does not reach Main Street, but flows back through the existing financial plumbing to fuel asset bubbles in stock markets. Economists and politicians wonder why all the new money created leads not to inflation but deflation. Instead, these pipes in the financial plumbing rarely reaches into local markets and individual spending, causing dangers of persistent deflation and recessions or what former fed Chair Ben Bernanke saw as a “glut of savings” and Lawrence Summers mystified as “secular stagnation”. Stock markets have come to expect the Fed to continue its QE and when it tries to taper it off, markets drop — in “taper tantrums”!

Today, the money meme is exposed, as millions see it being printed on TV. Israeli philosopher Yuval Harari in his “Homo Deus” (2017) and “Twenty Lessons for the 21st Century” (2018), calls out the money meme as the most successful myth of market fundamentalism and similar to most other religions beliefs. Harari describes the role of all myths and stories we humans create, so as to coordinate our efforts and social goals. Today’s popular movements in most democracies, see this money meme as exacerbating unfairness and inequality. Media show elites in their private planes at the World Economic Forum, Davos and other resorts. People and communities in “fly-over country” and rust-belts, experience widening poverty gaps, stagnant wages and disappearing middle classes, as unions are targeted by corporations and their political supporters. In European countries where the “occupy” movements began and in the USA, fairness is the battle cry. Following the 2008 debacles, as reckless bankers evaded prosecution, both the US right-wing Tea Party and the protesters at Occupy Wall Street carried similar hand-lettered signs “Where’s MY Bailout?” The global non-profit research group, Focus on the Global South, based in Bangkok, reports on “Rogue Capitalism and The Financialization of Territories and Nature” (2020), tracing how the world’s biggest banks, investment firms, insurance companies and even pension funds over-ride local communities and ecosystems and keep their assets in unregulated off-shore financial and tax havens. The group’s founder Prof. Walden Bello, former Philippines legislator, advocates that developing countries withdraw from the World Bank and IMF in his “Time for an Exit Strategy for the Global South?” (2020). I stress in all my books that companies are puppets of finance and these global banks and institutional investors, private equity, and family offices. This is why Ethical Markets follows finance, as I do in “Ethical Markets: Growing the Green Economy”, (2007)

In 2020, as the COVID-19 virus-related lockdowns decimated consumer-driven economies, it upended the old-time economic textbooks focusing on debt, deficits, inflation fears, and GDP. Instead of budget and job cuts, “austerity” and moralizing on belt-tightening to save our children’s debt burdens, the new slogan was “stimulus“ tax refunds, negative interest rates to combat deflation and another depression. In the space of a few months, the Fed created $7 trillion of new money and Congress passed the March 2020 $4 trillion COVID-19 relief bill. This swift, bi-partisan stimulus kept unemployed consumers spending and paying their bills, flowing into aggregate demand, including the direct payments to businesses of all sizes according to their funding of lobbying power, along with $2000 Treasury checks to millions of individuals, prominently signed by Donald Trump.

Later in 2020, as Congress passed in April another $3.1 trillion bill, the Senate baulked as market fundamentalists’ textbook models still warned of rampant inflation, while deflation still loomed. The financial plumbing blocked much of this new money from flowing to the poor people policymakers needed to spend it into the economy. Instead, it flowed to the rich who saved it or sent it offshore to their tax havens, while corporations used these free funds to buy back their stock. The V-shaped recoveries predicted in orthodox theory became the unequal K-shaped recovery of late 2020. The money meme failed in every US state and municipal government. These local governments, unlike the national governments and Fed, are unable to print their own dollars. They must rely on national legislators. In the US, all states need Congress and its fiscal powers, as they battle the COVID-19 virus with overflowing hospitals, loss of local tax payments while paying out funds to their unemployed and trying to keep first responders on the job in all their vital public services. Republicans revived the debate on deficits, vacillating on the new stimulus needed and refused to take up the additional $3.1 trillion Congress had passed in April, 2020.

Yet, the Fed is actually authorized to buy the sovereign bonds issued by all US states, rather than only dud mortgages  securitized in bonds — all those new financial vehicles created to sell them to unsuspecting school districts, as well as in European countries. In California, hurt also by climate-related droughts and fires, a coalition of non-profits, NGOs, academics, businesses and Green New Deal supporters emerged. One of the demands was for the Fed to use some of its new money to buy California’s sovereign bonds and help restore the COVID-related budget shortfalls. Monetary experts, Ellen Brown, Robert Hocking and others agree with me and Nathan Tarkus, in his 2020 paper “Is It Legal for the Federal Reserve to Provide State and Local Governments Unlimited Credit Lines?”, that states and local governments should issue their own complementary currencies, allowed in other countries, as they did in the USA, Canada and Mexico during the Great Depression, documented with illustrations in “Standard Catalog of Depression Scrip of the United States in the 1930s“ (1961, now out of print). We also urged that the Fed stop fearing to use its authority and to also buy states’ sovereign bonds prevent firing essential workers and massive declines in vital public services.

securitized in bonds — all those new financial vehicles created to sell them to unsuspecting school districts, as well as in European countries. In California, hurt also by climate-related droughts and fires, a coalition of non-profits, NGOs, academics, businesses and Green New Deal supporters emerged. One of the demands was for the Fed to use some of its new money to buy California’s sovereign bonds and help restore the COVID-related budget shortfalls. Monetary experts, Ellen Brown, Robert Hocking and others agree with me and Nathan Tarkus, in his 2020 paper “Is It Legal for the Federal Reserve to Provide State and Local Governments Unlimited Credit Lines?”, that states and local governments should issue their own complementary currencies, allowed in other countries, as they did in the USA, Canada and Mexico during the Great Depression, documented with illustrations in “Standard Catalog of Depression Scrip of the United States in the 1930s“ (1961, now out of print). We also urged that the Fed stop fearing to use its authority and to also buy states’ sovereign bonds prevent firing essential workers and massive declines in vital public services.

While markets and all forms of useful trading will continue in all societies ,they still need to be limited, steered by social norms, with excesses curbed by enforcing regulations, as I describe in “Markets’ Problem Twins: Trading and Advertising”. Economists’ fantasies of “market completion “i.e. spreading use of money to mediate all human transactions, are revealed. Money serves individualism, on which market economics is based. The multiple market failures in financial globalization were exposed by former World Bank economist Nicholas Stern‘s, “The Stern Report” (2006), seeing climate disruption as the biggest market failure in human history, as social and environmental costs “externalized” from government and business balance sheets reached the IMF’s worldwide estimate of $5 trillion annually . These hidden costs, risks and dangers of market failures, now further revealed in the global pandemic, drive recognition of the limits of the money meme. Narrow, money -based transactions cannot continue to dominate all other values of health, education, equality, justice, fairness and environmental quality, as I describe in “Steering Societies Beyond GDP to the SDGs”, the Sustainable Development Goals ratified by 195 countries at the UN in 2015. This new systemic set of goals and science-based indicators embrace the grassroots-developed targets for human development in the planetary realities and risks that we humans face going forward. I and my colleague, physicist Fritjof Capra acknowledge these risks as self-inflicted by our limited perspectives in our positive scenario “Pandemics: Lessons Looking Back From 2050” describing all the available tools we already have to steer our societies toward peaceful sustainable futures. Formerly outside-the-box proposals by Milton Friedman in the 1960s of “negative income taxes” re-emerged in 2020 in US election platforms including Andrew Yang’s universal basic incomes and using direct dispersing of “helicopter money” as optimal forms of stimulus!

The opening of closed minds by the pandemic reversed many obsolete paradigms, while scientific research in many fields had already invalidated most of the tenets and concepts of economics as I described in “Mapping the Global Transition to the Solar Age: From Economism to Earth Systems Science, (2014), with a Foreword by NASA Chief Scientist, Dennis Bushnell. Modern Monetary Theory (MMT), based at the Levy Institute, at New York’s Bard College, (www.levy.org) emerged in 2020. The most articulate spokesperson is Prof. Stephanie Kelton, former chief economist of the U.S. Senate Budget Committee, now chair of the Department of Economics at University of Missouri Kansas City, in her “The Deficit Myth”, (2019). She focuses on the widespread misunderstanding and miscasting of debts and deficits, as politicized money-based arguments to prevent needed public investments, social services and infrastructure, as the USA grew into a nation with 330 million people.

Of course deficits matter! But so do the public and private assets they create: schools, hospitals, roads, bridges, dams, broadband, R & D, as well as military weapons, the VA, Social Security, Medicare and public health plans to counter pandemics! Why do we all lose sight of these valuable assets? Partly because GDP in addition to its other failures, does not have an asset account, as is proper in double-entry accounting. Instead, GDP is a cash-flow statement, and ignores all these public assets created by Congress which are vital investments underpinning all modern societies, which balance out the debits. Another example in GDP: education is classified as “consumption” (along with hamburgers and ice cream cones). Yet, we know that educating the next generation of healthy knowledgeable citizens is the most important investment all democratic societies make in their future!

All these errors in money-based GDP and macroeconomic statistics concealed in algorithms lead to false signals to investors, pension fund managers worldwide, which manage our societies, retirement benefits and our childrens’ future. Asset managers worldwide follow inflated “debt-to GDP ratios” which still ignore the value of the public assets these investments have created. If these assets were recognized and included, many countries’ would have their “debt-to-GDP ratios“ cut by up to 50% with a few keystrokes! Similarly, proponents of the USA’s “ Green New Deal” and in Europe’s “Green Deal” point out that such mega-investments were created in the New Deal during the Great Depression, such as the massive Hoover Dam — without which Los Angeles would still be a village!

Such financing can only be provided by governments, which can create the guarantees, bonds and public contracts on which companies can then bid to build such national infrastructure. They include the US interstate highway system launched in the 1960s and President John F. Kennedy’s Mission to the Moon. The absurd ideas of the market fundamentalists that such “moonshots” can be funded by private companies and passing the hat among taxpayers are revealed by MMT theorists. Indeed, these investments underpin future prosperity, create all the new technologies, industries and jobs, while assuring adequate education, healthcare, extending assistance and safety-nets, as well as supporting workers displaces in obsolete, fossilized sectors as societies continue their global transitioning to the renewably-resourced, circular economies, as we cover in our Green Transition Scoreboard® and forthcoming e-textbook. “Mapping the Global Green Transition, 2009-2020.

These global transitions include structural and cultural shifts toward to systemic SDGs are all viable with existing technologies and are achievable within the ten-year window advised by the UN’s IPCC to reduce CO2 emissions to stay within their 1.5 -2 C degrees of global warming. With our cleaner understanding of the money-meme, we can put markets and money in their rightful place. As I document in “Paradigms in Progress: Life Beyond Economics, (1990, 1996) and “Building a Win Win World, (1996, 2004 e-book). We can ban “fraudulent externalities” with correct metrics of full-spectrum accounting internalizing all forms of global pollution and health risks, shifting risky old investments to the scaled up, cheaper use of renewables. All this corrected accounting reveals ways of avoiding many current costs. Shifting from GDP which incentivizes bad behavior (the Seven Deadly Sins!) toward the SDGs can again reinforce our traditional community sectors of sharing, caring and the Golden Rule we were taught and teach our children, as we describe in “Transitioning to Science-Based Investing” (2019-2020).

**********************

Hazel Henderson, global futurist, science policy advisor and author of Building a Win-Win World: Life Beyond Global Economic Warfare (1996, 2014 e-book) is CEO of Ethical Markets Media Certified B Corporation publisher of the Green Transition Scoreboard® and producers of the TV Series, “Transforming Finance” distributed globally to colleges and libraries.

Hazel Henderson, global futurist, science policy advisor and author of Building a Win-Win World: Life Beyond Global Economic Warfare (1996, 2014 e-book) is CEO of Ethical Markets Media Certified B Corporation publisher of the Green Transition Scoreboard® and producers of the TV Series, “Transforming Finance” distributed globally to colleges and libraries.