Global regulation is coming? — US encourages collaboration — Wealthfront’s disruptive potential

Sarah Kocianski and Jaime Toplin | April 04, 2016

Welcome to Fintech Briefing, a morning email providing the latest news, data, and insight into the developing fintech ecosystem in Europe and around the world, produced by BI Intelligence.

Did someone forward you this email? Sign up and receive Fintech Briefing to your inbox.

HELP MAKE US BETTER. When you’ve finished reading, don’t forget to rate this edition of Fintech Briefing on the scale at the bottom.

CENTRAL BANKERS TO EVALUATE FINTECH RISKS: Last month, Mark Carney, Chairman of the G20 Financial Stability Board (FSB), informed G20 finance ministers that the FSB would begin evaluating the risks posed by fintech to global financial stability. Last week, the FSB proposed a framework for categorising major areas of fintech and evaluating each area’s potential risks to consumers, public authorities, and financial stability.

Regulators can no longer ignore the fintech industry. It’s become clear that fintech will disrupt more than one element of the financial services ecosystem. A third of bank workers could lose their jobs, traditional financial services firms expect to lose up to 20% of their business, and consumers may be exposed to increased risk of financial losses.

The FSB works with regulators. The FSB is made up of central bankers, regulators and financial ministry officials from G20 countries and other key financial centres. It sets non-legally binding policies and minimum standards that members agree to implement at a national level. As it investigates fintech, the FSB will engage with global regulators to get a better understanding of the industry and different regulatory approaches.

That could lead to a global regulatory approach to fintech — and that might not be a good thing. A global approach could be bad for fintechs if categorisation of fintechs is overly broad. Fintech categories that are classed as high risk could be subject to heavier regulation and nuances in business models may be overlooked. That could mean some areas may be stifled globally, while others flourish.

US REGULATOR PROMOTES COLLABORATION: The US has different financial regulation at state and federal (national) levels, and no coherent regulatory policy on fintech. This makes it hard for fintechs to know if they are operating within the law, and inhibits partnerships with traditional financial institutions. Last week a federal regulator, the Office of the Comptroller of the Currency (OCC), issued eight guiding principles for developing a framework designed to help simplify the situation. The guiding principles fit into four areas: Fostering financial innovation consistent with sound risk management; protecting consumers; promoting collaboration; and improving communication.

This looks good for fintechs for three reasons:

- Communication channels between fintechs and regulators are vital to developing supportive regulation. They enable regulators to understand the nuances of differing fintech business models and take them into account when regulating. And they give fintechs an avenue to address issues, concerns or questions around regulation. Another US regulator, Securities and Exchange Commission Chair Mary Jo White, also confirmed the importance of communication between the fintech community and policy makers last week during an event in Silicon Valley designed to encourage the two groups to work together.

- Clarification of requirements would benefit fintechs and incumbents. During the OCC’s consultation, financial institutions and fintechs both said that regulators’ requirements around partnerships between the two groups were unclear. Clarification would make both groups more likely to partner, allowing fintechs to benefit from banks’ scale and resources, and banks to access technology without resorting to acquisition.

- Collaboration across state, federal and international regulatory bodies is key to promote consistency. The OCC has said it will work with bodies like the Consumer Financial Protection Bureau (CFPB) to ensure the regulatory burden on firms wanting to innovate isn’t onerous and is applied consistently. Having one set of regulations to adhere to across the US would make it easier for fintechs to grow.

WEALTHFRONT OFFERS PERSONAL FINANCIAL MANAGMENT FEATURES: Last week, robo-advisor Wealthfront announced its intention to progress from pure investment advice into personal finance management. Users can now create a dashboard (pictured below) where they can see all their financial products – including bank accounts, mortgages, and payments products like Venmo – in one place. It will then take that data and use it to give users a projection of their net worth, and over time give financial advice over “diversification, taxes and fees” tailored to that user’s standing and preferences. Wealthfront launched in 2011 with an automated investment offering that uses an algorithm to choose the best investments for consumers.

Robo-advisors threaten more than just the wealth management industry. As robo-advisors apply their technology to consumers’ entire finances, rather than just their investments, they could become intermediaries between banks and their customers, and perhaps even disintermediate banks altogether.

P2P LENDING ISN’T SO TRANSPARENT: Many P2P lenders publish details of their loans and cite it as evidence of how transparent they are. They say that transparency makes it easier for investors to understand the risks involved in P2P lending. But publishing loan details doesn’t necessarily lead to a clear presentation of risk. For example, the FT investigated a number of P2P lender Ratesetter’s loans and found that, due to mislabeling, the information presented was actually quite opaque, according to FT Alphaville. That suggests that P2P lenders’ “transparency” isn’t necessarily the selling point they claim and could actually damage the industry. If regulators find that the data on P2P platforms is misleading they may introducing prohibitive regulation to protect consumers.

Adopting a common standard for data could be an alternative to regulation. Companies like AltFi Data, have developed ways of standardising the data to make it easier to understand and compare. If AltFi Data succeeds in becoming recognised across the industry, it could lead to all lenders offering data in the same format — which would make it easier for consumers to evaluate risk.

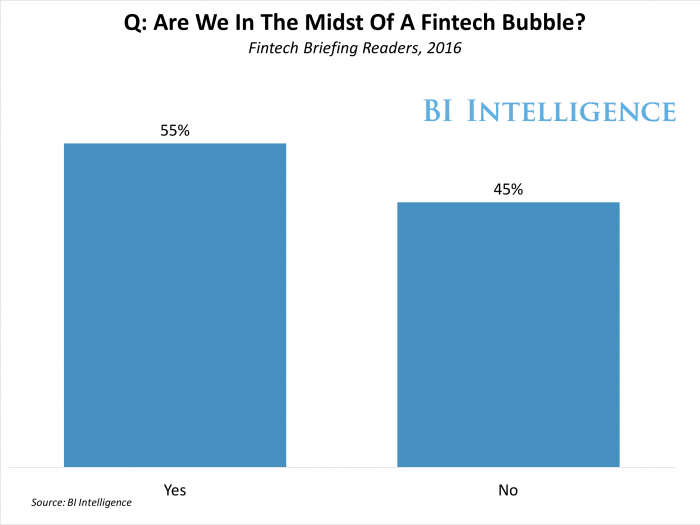

RESULTS OF WEDNESDAY’S SURVEY: Last Wednesday we asked “Is fintech in the midst of a funding bubble?” Here are the results

Around the world…

SINGAPORE LAUNCHES FINTECH HUB: Singapore recently laid out its Smart Nation initiative, designed to encourage innovation in the country. As part of the initiative, the government will set up a fintech hub, according to Finextra. It will give fintechs access to talent from key research institutions and introduce them to investors. Singapore has all the ingredients needed for a successful fintech industry — talent, ideas, and supportive regulators — but struggles to attract investors because it fails to combine these resources into viable investment opportunities, according to EY. Singapore hopes that providing an environment dedicated to collaboration will solve this problem.

ALTERNATIVE LENDING STARTUP CLOSES £6.4 MILLION ROUND: Branch, a financial firm that offers mobile money-based lending options to people in developing nations, announced the close of a £6.4 million ($9.2 million) Series A funding round, led by Andreessen Horowitz. Branch, which is currently live in Kenya, uses data stored on users’ mobile phones, like contact lists, social data, and SMS logs, to assess credit, approve users for loans, and offer them to customers. If approved, funds are distributed instantly through M-PESA accounts. Users also repay their loans through M-PESA, which allows them to build credit going forward. Branch plans to use the new funding to expand into new countries, like Tanzania, as soon as possible.